In the past year or so of my life, I’ve spent a large chunk of time organizing how I store and spend my money. Some of my friends have asked me to give an overview of my “setup” as it stands in the year 2020, but it’s complex enough that I think writing something is in order.

If you are reading this and you think my ideas are dumb, you should also let me know! I’m always looking to do stuff better.

Before understanding what I do, I think it makes sense to preface with a “why do I think this way.” If you don’t care or think you are more financially literate than a dummy like me, feel free to skip to below.

Storing Money

One of the first obvious needs that most people have is storing their money. You probably get a paycheck — where should you put it? The worst thing you could do is store it somewhere that it doesn’t get any interest; however, I don’t think the best option is necessarily storing your money somewhere that has a high interest rate, as there are usually some stipulations to doing so. There’s a couple of high-level concepts that I thought about when making this decision, and weighing these trade-offs.

Upside and downside

When it comes to managing risk in your investments, one of the key questions to ask is: what is the upside and what is the downside of such an action?

As a quick tangent — this question is one of the biggest takeaways I’ve had from the incredibly dense book Antifragile by the self-absorbed author Nassim Taleb. While it isn’t a fun or easy read, developing an intuition on how to apply ideas like this makes me think that it is worth slogging through.

When it comes to simple money management, I think most people fail to consider both sides of this question. Many people say something like “put your money in an index fund, follow the S&P500, put it in a brokerage account.” While I don’t think this is always bad advice, I think it should always come with a very clear footnote: these forms of investment could make you lose money.

Putting your money into an account like VOO, SPY, or IVV that mirrors the S&P500 (an index reflecting the performance of the stocks from 500 large US companies) means that if the stock market crashes, you will lose money. Some people dismiss this with statements like the S&P500 has a historical average of 10% year over year growth. And while this is true, it is historical data, and it does not definitively predict the future. It also brushes off that you might want or need to withdraw money in a downturn, and you can’t wait.

Maybe we live in a world where the US has a recession, never really recovers, and other countries like China take our place a world superpower. The S&P500 wouldn’t be doing so hot then.

This isn’t to say that’s my prediction for our future, but rather that if I want a guarantee of not losing my money, I need to store my money in some form that has a strictly capped downside.

Some example of this might include things like High Yield Savings (HYS) accounts or Certificates of Deposits (CDs). You cannot lose money on these methods of storing capital; you can only gain interest.

That also being said, the upside of these types of investments is usually lower than other methods, as well as a fixed cap. That is, if you pick a 3% APY CD, it won’t return you more than that.

Using the stock market as a comparison again, this means the trade-off on not being able to lose money is not being able to capitalize on large (or even near limitless) upside. The best stock investment I ever made I ended up selling at a 238% increase. That is simply not possible with something like a HYS or a CD. However, I did not know that this would happen. I got lucky; I could have been unlucky.

How much are you willing to gamble?

Liquidation and Waiting

Another consideration of storing your money — how much do you want to spend, and when do you want to spend it? With some forms of monetary storage, like CDs, there are penalties for taking your money out early (you agree to let it sit for a certain number of years.) Or with other investments, like a stock index fund, if you are currently at a loss, it might not make sense to sell yet. It might be better to hold longer in hopes of you ultimately ending at a net positive. Indexes can also get complicated because of the tax implications like capital gains; I won’t get too in-depth here, but just realize pulling money in and out of certain investment stores is time-intensive and costly if you don’t do it right.

Some people use the rule of thumb that you should have “6 months of runway” in a fairly easy to access form of monetary storage at all times. I don’t like rules like this, because it doesn’t show the thought process of the mantra. However, I think the concept they are trying to touch upon is that most people need to be able to liquidate quickly, and it could cause them to lose more money if they can’t play the waiting game with other investment vehicles.

I don’t think there’s a catch all answer on how much to keep liquid. I’ll go over my personal approach to this later on, but generally I think it comes from a place of understanding what your future spending should look like.

Beating Inflation

The inflation rate has been roughly ~2% each year for the past decade or so. This means that even a HYS with 2% APY might not truly help you gain money. In some sense, if things are becoming more expensive each year, the numeric growth of your bank account might only maintain your spending power, not increase it.

One could argue that the calculated inflation doesn’t reflect the realities of your life; I to some degree believe this. Inflation is calculated based on a consumer price index (CPI) which is based on a “basket of goods” concept — this is, what are the common items people spend money on, and how do those prices change over time?

But how does the cost of living change where you live? Do you buy things that most people buy?

I digress. Prices do keep increasing (we can argue about at what rate) and therefore, you need your money to also passively increase, else you effectively have less money.

Bimodal Investing Strategies

Some of the above ideas are in direct conflict. Most ways you can store your money that have a capped downside also have a lower upside — specifically, the rate is probably less than or around inflation. So if the only thing you do is put your money in a HYS, you won’t actually be growing your spending power (in relation to the cost of living.)

However, you still probably don’t want to open yourself to the risk of losing most of your money, and you also probably want to be able to spend at least some amount of money regularly.

The answer here is a bimodal investment strategy. For example, keep 90% of your money in more liquid stores of capital, with some but not a lot of interest. For the other 10%, go crazy. Invest in something you can lose all of your money in. Invest in something with an uncapped upside, where the return can be some multiplier of what you put in.

For many people, they can’t stomach “might lose it all” risk. I do want to be clear though, technically speaking, there is still some chance you can lose it all in the stock market. That said, on an intuitive level, it’s probably less risky to put your money in a brokerage account following a well-known index versus dumping all of your money into very specific investments.

Because of this fact that many investments truly don’t have a capped downside, many brokerage accounts will try mitigating risk by spreading investments across many monetary stores. If you are savvy (and I would argue if you want to be rich) you should try to pick some investments to diversify across for yourself. Otherwise, many services do this for you. For example, my Wealthfront robo-advisor splits the portfolio into US stocks, foreign stocks, emerging markets, dividend growth stocks, and municipal bonds.

Because of the nature of things that can have a multiplier of growth, and have no real limit to their upside, it makes a lot of sense to have some diversification. For example, if you put $1 into investment X, it might turn into $1,000, or $10, or you might even lose the dollar. If you really don’t know the odds (or lack a strong intuition) about how that investment might grow, it could make more sense to take your $1 and put 10% into investments A, B, C, D, etc, since it is effectively a lottery. You really want more chances at winning the lottery.

However — I advocate for having some conviction in some investments. You don’t want to feel bad when you only put $1 into something that grew 100x if you could’ve put $1000 and now have been a millionaire.

If you want, be your own judge of what is safe versus risky. But split your money between the two conscientiously. Have your “safe” stores of money (401k, HYS, etc,) and your “risky” stores that you are at least partially diversified in (but don’t be afraid to unevenly diversify to place bigger bets in some areas you strongly believe will win.)

Spending Money

I don’t think a lot of financial guides talk about this, but in my opinion, it’s almost just as important as saving your money well.

The Federal Reserve Bank of Boston has an interesting analysis where they describe how credit card users effectively leech money from cash users (which also tends to be rich people using credit cards, and poor people using cash.)

Let’s say a merchant is selling an item for $1.00. They want to accept credit cards for sales of this item, but credit card companies make merchants pay a fee that is a percent of the total cost. So this $1.00 item might cost the merchant $1.01 to $1.04 including the credit card fees. So to combat this, merchants raise the price of the item. They can’t only make credit card users pay more though; this is against the terms of service for accepting credit cards. So now everyone buying this item pays $1.04, even though it could in theory be priced at $1.00.

Where this gets interesting is that credit card users usually have a cash back program nowadays. So while I “spend” $1.04, I might have 4% on food purchases, so I’m effectively spending less money. Cash users who do not get the percent back are effectively paying more for the same service.

On top of this, many credit cards have sign-up bonuses, many of which are worth $500+.

On the most extreme end of this arbitrage, you have people known as credit card churners who open multiple credit cards for the bonuses, then close the cards ASAP after meeting the minimum spend requirement. I was recently chatting with someone who has opened 43 credit cards. There are even flowcharts on what order to apply for cards to maximize the benefits. If this is a topic of interest to you, you should read more on r/churning on reddit.

While churning can be extreme and too time consuming for many people, at least trying to maximize on how you choose to buy things can easily save you 1% a year on nearly every expense, if not much more. I personally have gotten thousands of dollars in sign up bonuses, and probably 3-4% back on my purchases.

I buy a lot of stuff, but I probably spend less money than people who buy the same things I do.

(As an side but out of the scope of this article: coupons and other programs like Ebates can further discount what you buy. I admit I could do even more research here than I have, but a lot of this is simple to do and can get you decent money back. One of my favorite quick tips is to sign-up for newsletters for coupons using 10 Minute Mail’s temporary email address. Get the “15% off for new customers” coupon without the spammy emails.)

Credit cards, loans, and other forms of segmented payback methods, also offer other indirect benefits. The ability to pay off items at no interest, or incredibly low interest rates, can allow you to use your liquid assets to do other things that might make you more money than you “lose” from interest.

A very common example of this is student loans. Many financial advisors (or at least the many I have talked to) are in agreement that if your loan’s rate is sufficiently low, if you had an extra $10k, you should probably invest it in a way that you make more interest than you pay on your loan, and then just continue with your minimum payments.

Intuitively it makes sense to spend your money to pay off debt. But if your debt allows you to make more money than you are in debt, it’s a great thing. (It also is good for your credit score.) If your student loans are at a 3% APR and you intend to keep the loan for 20 years, you might as well take the extra money that could have gone towards that loan and get 10% on something else, since the net is positive. In short — don’t always spend money to pay off debt.

My Financial Process

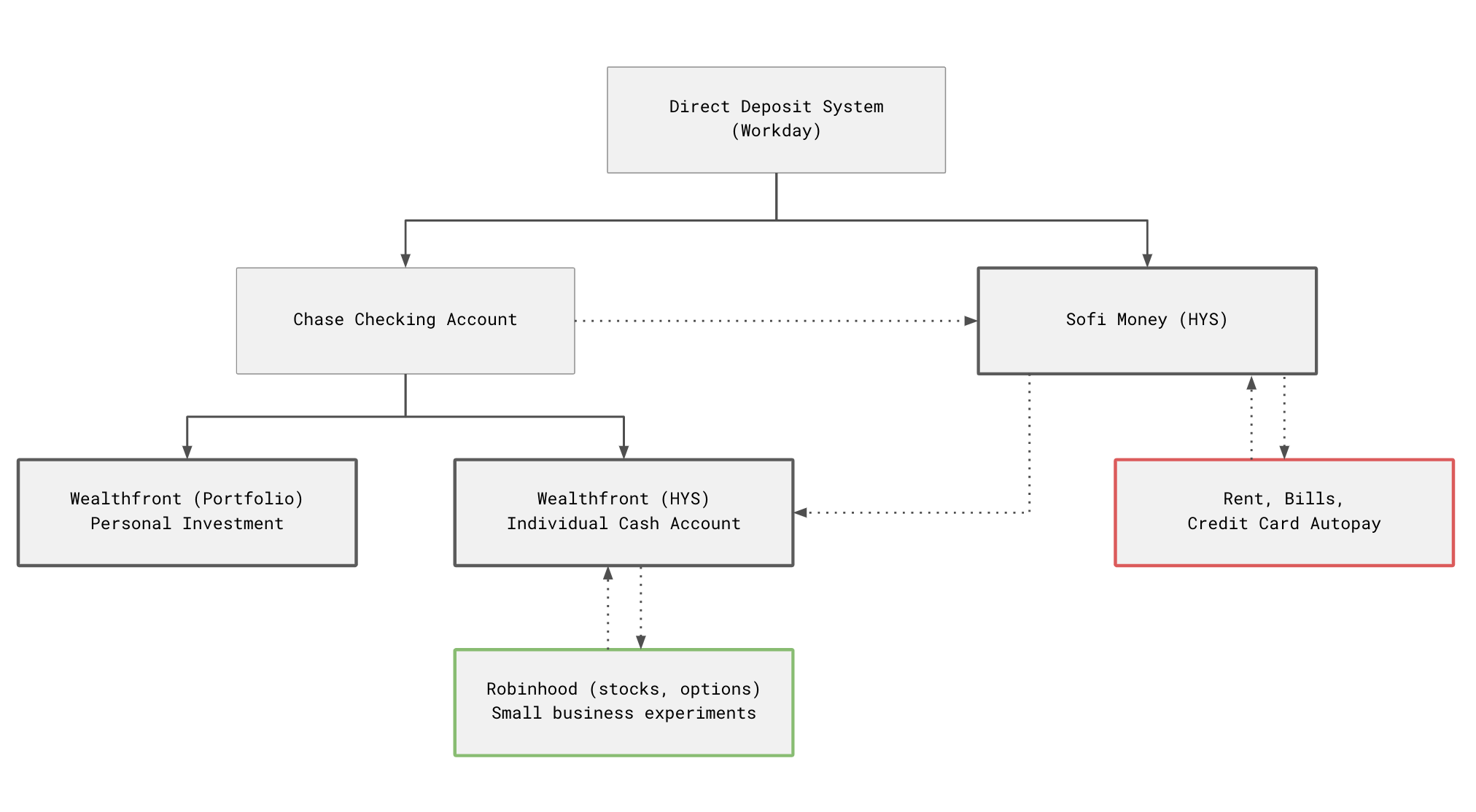

My employer uses Workday to have employees specify where their money gets direct deposited into. Workday (and many other systems) let you pick more than one place to send your money, and you can even split by a specific dollar amount or by percentage of your pay check.

After deductions like 401k contributions and other pre-tax benefits (gotta love using stuff like commuter benefits where possible,) I have my paycheck go to two places: a Chase checking account and a SoFi Money online checking/HYS combo.

(Side note: if you want free money, this referral link for SoFi Money gives you and I both $25 once you deposit your first $100.)

Why do I have it split into two places? A few reasons.

At a high-level, reflecting back on my principles for how to store money, I want a substantial amount of my money in a very liquid, but high-as-possible interest earning accounts. That led me to look into a bunch of online bank accounts that have the highest interest rates. While at a first glance, the main difference between them all is the interest rate, there are a two other features that I think are valuable to look for.

- does the account have a routing number (without which, you won’t be able to set up direct deposit)

- does the account offer a debit card with ATM access

The second piece is actually a bit trickier than one would think. To my understanding, there is not an online high yield account that offers you the ability to actually deposit cash into an ATM. You can only withdraw money. So whenever I come across cash, if I only opted to only have an online account, I would not be able to easily get rid of the cash.

Beyond ATM cash deposits, I can’t really think of a good reason to use Chase/Wells Fargo/Bank of America checking or savings accounts. However, if you leave these accounts mostly unused, then they will charge you “usage fees.”

In an ideal world, I would pick whatever savings account had the highest APY (which from my research, seem to be Wealthfront and Betterment) and I would be able to deposit my paycheck and use an ATM to deposit and withdraw into these accounts. These functions aren’t available for these accounts, so I had to compromise a bit.

SoFi has an online HYS/checking combo account (called SoFi Money) that has routing numbers (that is, you can direct deposit to them) and has a withdraw-only debit card, but still a fairly high APY. That makes it a pretty good option to use as a central checking account.

SoFi Money’s debit card also refunds all ATM fees you incur on the card. This makes it very flexible for getting money in foreign countries or odd ATM locations like niche bars or concerts with nortiously high fees.

In order to still keep the functionality of depositing cash via ATM, I kept my Chase account, and send some portion of my paycheck that meets the minimum direct deposit amount needed to waive all fees. I mostly use it as a pass-through though. I have Wealthfront scheduled to pull money from this account right after the paycheck hits, so money rarely sits in Chase. This is important to me because Chase checking yields no interest. If for some reason there exists more money in Chase than Wealthfront pulled (maybe because I deposited cash at an ATM,) I’ll transfer it to my SoFi account so that it can have additional interest.

Despite getting somewhat high interest on my SoFi account, it is mostly an account to serve as a hub between many other financial services. Nonetheless, the high APY is important to me because I can have large amounts of money floating in this account. If I don’t transfer out my paycheck quickly, and have other forms of money flowing in, I’m still not wasting much of the money’s potential by letting it sit there.

Wealthfront is my slightly longer term, but mostly liquid, storage of money. When my funds in SoFi start building up, I move them into Wealthfront. Also, as I mentioned before, I have Wealthfron also automatically pull money from Chase every paycheck cycle. I have two accounts with Wealthfront: one is a HYS, the other is a robo-investor portfolio. The rates for the HYS are slightly better than SoFi Money, so I might as well get another 0.2% for free (it used to be a bigger gap, but the Federal funds rate has changed.) The portfolio is also pretty customizable, and has a decent performance history. There are also no fees on your initial investments, and low fees on the rest; most in-person investors take large fees, so robo-investors have the potential to perform worse but still make you more money.

I generally put a small part of my paycheck into my Wealthfront portfolio each month, as opposed to dumping a larger chunk every once in awhile, because in theory this limits the effects of volatility on your investment (what people often refer to as dollar cost averaging.)

The plurality of my money is in Wealthfront’s HYS. I value flexibility, and think a stock market crash is believably likely. I also foresee needing a lot of liquid capital on-hand for upcoming parts of my life. The second-largest plurality of my money is with Wealthfront’s robo-investor portfolio.

If you want $5000 of assets managed with Wealthfront’s robo-investor without a fee, here’s a referral link.

For much riskier investments, I will often use Robinhood to buy specific stocks or options. If you haven’t signed up for Robinhood yet, you can sign-up and get a free stock (chosen at random) with this referral link. I have no special advice for how to buy/sell stocks and options well; you just have to read a lot about the topics and make educated gut decisions.

(Side note — Aren’t referral links fun?)

When I cash out of Robinhood, I often will put that money into SoFi (the hub of my money,) but will usually then transfer it directly into Wealthfront. Because Wealthfront lacks routing numbers, you can’t always do direct transfer. Similarly, I will occasionally cash out credit card points (especially on cards like the Uber Card where the redemption value doesn’t increase on certain items, in the same way it does for Chase or AMEX with travel) and send that to SoFi, but often with the end goal of putting it in Wealthfront for the few percent points of interest.

My most frequently used card right now is the AMEX Gold card (referral,) because it has 4% back on restaurants worldwide, and on grocery stores in the US. This is the best food cash back program I am aware of. Usually I use these points on travel, but as occasionally as mentioned above, I transfer the points into cash and put it into a HYS. Beyond my AMEX card, I’m mostly following the churning flowchart linked above to decide which cards to get next.

The riskiest investments I make are actually in my own random “business ideas.” I have (and am continuing to) play around with e-commerce, drop shipping, freelance consulting, and some other stuff. This type of investment could end up being throwing away the money entirely, but does have the upside of potentially working well enough to provide another source of income. Stuff like this also requires liquid money on hand, hence my Wealthfront and SoFi HYS’s.

Overall what works for me might not work for everyone; however, with the principles and thought-processes I laid out, I hope some people find this useful for their own savings and lifestyle goals.